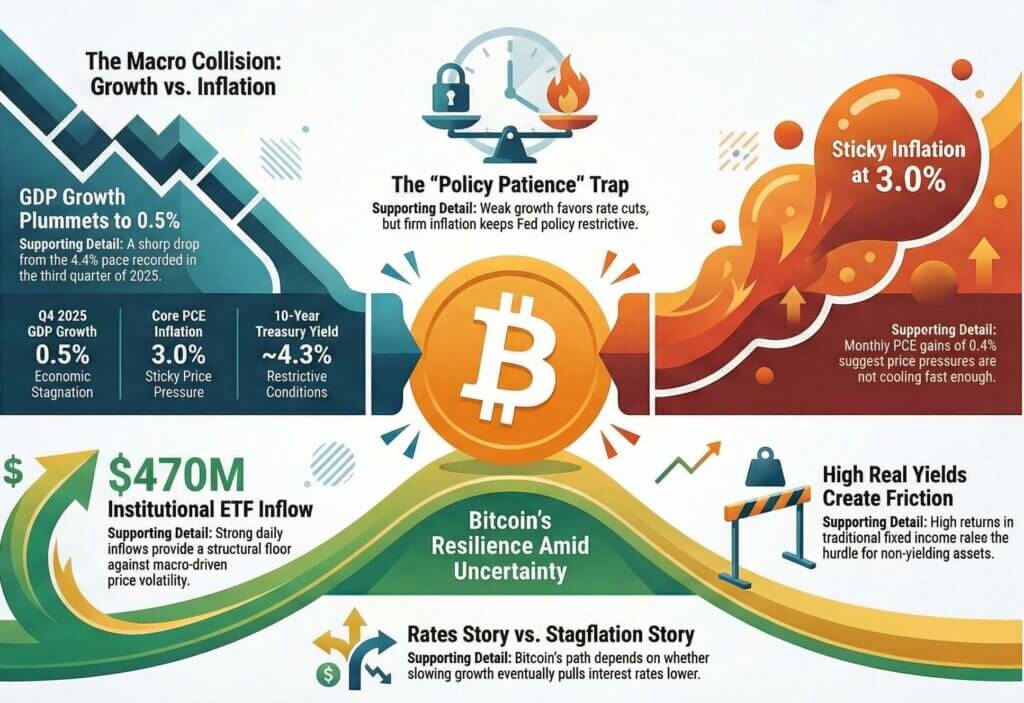

The U.S. economy entered 2026 with far less momentum than markets had priced in a few months earlier. According to the Bureau of Economic Analysis, fourth quarter 2025 GDP growth was revised down to 0.5%, a sharp step down from the 4.4% pace recorded in the third quarter.

On its own, that revision would usually support the view that the Federal Reserve is moving closer to rate cuts. The problem is that inflation has not cooled enough to give policymakers much room.

New PCE data released today shows headline inflation at 2.8% year-over-year in February, with core PCE at 3.0%. Monthly gains in both measures came in at 0.4%, a pace that still points to sticky price pressure rather than a fast return to the Fed’s 2% target.

That combination has become the real macro question for Bitcoin and the broader crypto market. Investors are dealing with an economy losing steam, while inflation remains firm enough to keep the Fed cautious.

The gap between the two trends has begun to shape the risk environment. It shapes the path of Treasury yields, the pricing of future rate cuts, and the willingness of investors to keep allocating into risk assets.

Bitcoin has already shown that it can attract capital amid difficult macro conditions, especially when exchange-traded fund demand remains firm, and supply remains structurally constrained. Even so, weaker growth does not automatically produce an easier backdrop for crypto.

The transmission channel runs through yields, liquidity, and confidence in the policy path.

MetricMost recentPrevious benchmarkU.S. real GDP growth, annualizedQ4 2025: 0.5%Q3 2025: 4.4%PCE inflation, YoYFeb. 2026: 2.8%Jan. 2026: 2.8%Core PCE inflation, YoYFeb. 2026: 3.0%Jan. 2026: 3.1%Bitcoin price$72,12924h: +1.20%, 7d: +7.84%, 30d: +1.43%

The GDP downgrade changed the macro setup for Bitcoin

As of press time, April 9, CryptoSlate’s Bitcoin price page has BTC trading at $71,201, down 0.72% over 24 hours, up 7.60% over seven days, and up 0.99% over the past month. That profile captures the current market state well.

Bitcoin has bounced, while the move has unfolded inside a macro environment that still feels unresolved. A weak GDP revision can appear to be a simple recession signal at first glance.

The larger point sits elsewhere. The downgrade landed at the same time that inflation remained elevated enough to keep the usual rescue mechanism out of immediate reach.

For Bitcoin, the next move still depends less on one growth print and more on whether incoming data can push rates and real yields lower in a durable way.

The 0.5% GDP reading challenged the idea that the U.S. economy was moving through a controlled slowdown with enough resilience to absorb tight policy and enough disinflation to bring borrowing costs down in an orderly way.

The sequence of official estimates, from the advance release to the second estimate and then the third estimate, showed a clear erosion of confidence around late-2025 growth. Markets can usually absorb a weak quarter when inflation is cooling fast enough for the Fed to step in.

This time, the inflation side of the equation has stayed stubborn enough to keep that path uncertain.

February’s PCE report intensified that problem. Headline PCE met expectations at 2.8% year over year, and core PCE came in slightly cooler than expected at 3.0% against a 3.1% consensus.

The monthly details were less comforting. Both headline and core increased 0.4% from the prior month, a pace that still leaves inflation running above where the Fed would want it if the central bank were preparing to pivot aggressively.

That is why the GDP revision and the inflation print belong in the same frame. The growth slowdown points toward easier policy. The inflation data keeps that outcome conditional.

Sticky inflation kept the Fed from offering easy relief

That tension also explains why the market response has been more complex than a standard reaction in which weak growth lifts hopes for faster easing. Treasury yields remain elevated enough to keep financial conditions restrictive.

The 10-year Treasury yield hovered around 4.3% after the GDP and PCE releases, while real yields have stayed high enough to preserve competition from safer assets. For Bitcoin, that creates a meaningful constraint.

Investors can still earn solid nominal and inflation-adjusted returns in traditional fixed income, which raises the hurdle for non-yielding assets. CryptoSlate recently framed this dynamic directly in its analysis of how Bitcoin trades real yields first.

That remains the clearest transmission mechanism here.

The labor market has added another layer to the picture. The latest BLS employment report showed March payroll growth of 178,000 and unemployment near 4.3%.

Weekly claims have moved higher at the margin, with the Department of Labor showing 219,000 initial jobless claims, yet the broader labor backdrop still looks resilient enough to give the Fed cover to wait. A labor market that is softening slowly, rather than cracking quickly, supports the case for policy patience.

Markets are therefore dealing with two incomplete signals at once: weaker growth and inflation that is still warm enough to keep caution in place.

For households, the practical consequence is straightforward. The economy is slowing, household costs still feel high, and interest-rate relief may take longer than many expected.

Mortgage rates, credit card costs, and consumer financing conditions all sit downstream of that same tension. Bitcoin enters this setup as a market that often benefits from looser liquidity, lower real interest rates, and a stronger appetite for alternative stores of value.

Those supports are only partially present right now. The GDP downgrade made the soft-landing narrative harder to defend.

It did not, on its own, deliver a clear all-clear for risk assets.

ETF demand is helping Bitcoin absorb a tougher macro backdrop

Bitcoin’s recent price behavior reflects that ambiguity. The asset has recovered enough to show that demand remains real, yet the move has not carried the kind of decisive follow-through that would signal a fully restored risk-on backdrop.

According to CryptoSlate’s BTC market data, the coin is up strongly on the week while remaining almost flat over the past month. That mix suggests a market willing to respond to supportive flows and tactical optimism, while still respecting that macro conditions have not yet resolved into a clearer pro-risk regime.

One reason Bitcoin has held up is the continuing support from spot ETFs. Spot Bitcoin ETFs drew roughly $470 million on April 6, one of the strongest inflow days of the year.

Those flows provide an important counterweight to macro pressure because they create a persistent source of demand from investors who are allocating through regulated products rather than trading short-term volatility directly on crypto-native venues. ETF demand does not erase macro risk.

It does change the asset’s resilience profile. A market with real institutional inflows can absorb more pressure than one driven purely by speculative leverage.

Still, the next phase depends on whether the slowdown becomes a rates story or a stagflation story. The distinction is critical.

A rates story would involve weaker growth gradually pulling yields and policy expectations lower, thereby improving the environment for Bitcoin, growth equities, and other duration-sensitive assets. A stagflation story would involve weaker growth alongside sticky inflation pressure that even re-accelerates, leaving the Fed constrained and risk assets facing a more difficult backdrop.

CryptoSlate’s recent explainer on why stagflation is becoming a market word again is useful here because it translates the jargon into something people already understand: costs stay high while the economy feels weaker.

Oil, inflation, and policy risk are colliding in the same window

That is where the outside-world collision becomes more important than any single crypto-specific catalyst. Energy is back in the macro conversation.

CryptoSlate recently noted that oil risk and reduced rate-cut expectations are starting to converge in the market narrative. If energy price pressures feed through into inflation expectations, the growth slowdown becomes harder for risk assets to celebrate.

The same weak GDP print that might usually lift hopes for faster easing could instead deepen concern that the Fed is losing room to respond.

Bitcoin fits into this environment through several layers. The first layer is policy expectations, which govern the path of front-end rates and shape broader liquidity conditions.

The second layer is real yields, which influence the opportunity cost of holding BTC. The third layer is structural crypto demand, particularly ETF inflows and spot accumulation. The fourth layer is risk sentiment, which determines whether markets interpret incoming data as easing-friendly or growth-threatening.

Bitcoin can perform well when one or two of those layers improve. Sustained upside usually becomes easier when three or more align.

Right now, structural demand looks constructive, while policy and rates remain mixed. That is why the market still feels lively rather than settled.

The slowdown has opened the door to a more supportive macro path for Bitcoin. The inflation data has kept that door only partially open.

The next test has a clearer roadmap; inflation, yields, ETF flows, and the incoming growth data will tell markets whether the 0.5% GDP print was a late-2025 air pocket or the start of something more durable.

The next 30 to 90 days will decide which side of the contradiction gives way first

The next quarter has enough scheduled data to force that choice. The immediate checkpoints are the next inflation releases, the April Federal Reserve meeting, and the first estimate of the first quarter GDP.

The Atlanta Fed’s GDPNow model will shape expectations into that report, while the Cleveland Fed’s inflation nowcast offers a live look at how sticky price pressure may remain before the official numbers arrive. These indicators keep the focus on what changes next rather than on a backward-looking debate over whether fourth-quarter weakness was large or merely surprising.

A constructive scenario for Bitcoin would start with a renewed disinflation trend. That could come from softer monthly CPI and PCE readings, easing energy pressure, or clearer signs that demand is cooling without a deep labor-market break.

In that setup, yields would have room to fall, Fed cuts would move closer in the market’s calendar, and Bitcoin would gain from a lower-rate environment while still enjoying structural support from ETF demand. The Federal Reserve’s March Summary of Economic Projections still points to 2.4% GDP growth in 2026, 2.7% PCE inflation, and a year-end fed funds rate of 3.4%.

Those numbers show that the official baseline still leans toward a slower but intact expansion. If incoming data moves in that direction, the current growth scare could become a bridge to easier conditions rather than a warning of broader deterioration.

A more difficult scenario would involve inflation staying close to current levels or moving higher again, especially if oil or other supply-driven pressures keep monthly prints firm. In that case, the growth slowdown would feel less like an invitation for policy relief and more like a constraint on the Fed.

Bitcoin could still attract demand as a scarce asset and as a hedge against long-term policy stress, yet the first-order market reaction would likely stay tied to broader risk sentiment. High real yields and delayed rate-cut expectations would continue to compete with the bullish structural case coming from ETFs and long-term accumulation.

There is also a middle path, and it may be the most realistic one over the next several weeks. Growth could stay soft without collapsing, inflation could cool slowly without offering immediate comfort, and Bitcoin could continue to grind inside a range where each positive impulse meets a macro counterweight.

That kind of market often frustrates directional conviction while still rewarding selective accumulation. It also tends to favor disciplined interpretation over dramatic conclusions.

The broader global backdrop reinforces the need for balance. The IMF’s latest World Economic Outlook update still projects global growth of 3.3% in 2026.

That keeps the U.S. slowdown in perspective. It is a serious signal, especially because it coincides with inflation that remains above target, yet it has not become a full-system global break.

Bitcoin sits in the middle of that distinction. It remains exposed to macro tightening and sensitive to real yields, while also benefiting from stronger market infrastructure, deeper institutional access, and a structural demand base that did not exist in prior cycles.

One conclusion stands above the rest. The GDP downgrade exposed real weakness in the soft-landing narrative.

The inflation data kept the Fed from offering immediate reassurance. Bitcoin is therefore trading an unresolved macro contradiction, one that will likely be settled by the next sequence of inflation, labor, and growth data rather than by today’s revision alone.

Growth has slowed sharply, inflation still has a grip on policy, and Bitcoin’s next sustained move will depend on which side of that tension gives way first.